")

Are you a property owner looking to expedite your path to financial success? If so, debt recycling could be the game-changer you’ve been seeking.

Debt recycling isn’t just a trendy term; it’s a strategic financial manoeuvre that empowers property owners to pay off non-deductible home loan debt while simultaneously leveraging equity to invest in income-generating assets. This savvy approach not only opens doors for claiming tax deductions on the new debt but also supercharges wealth creation.

The allure of debt recycling lies in its ability to expedite investments that would otherwise require years of saving. By harnessing debt in this manner, individuals can cultivate passive income streams and optimize tax deductions along their financial journey.

However, like any financial strategy, debt recycling isn’t without its risks. To navigate this terrain successfully, it’s vital to grasp the concept and its implications fully. Let’s delve deeper into the world of debt recycling.

Understanding Debt Recycling Strategy

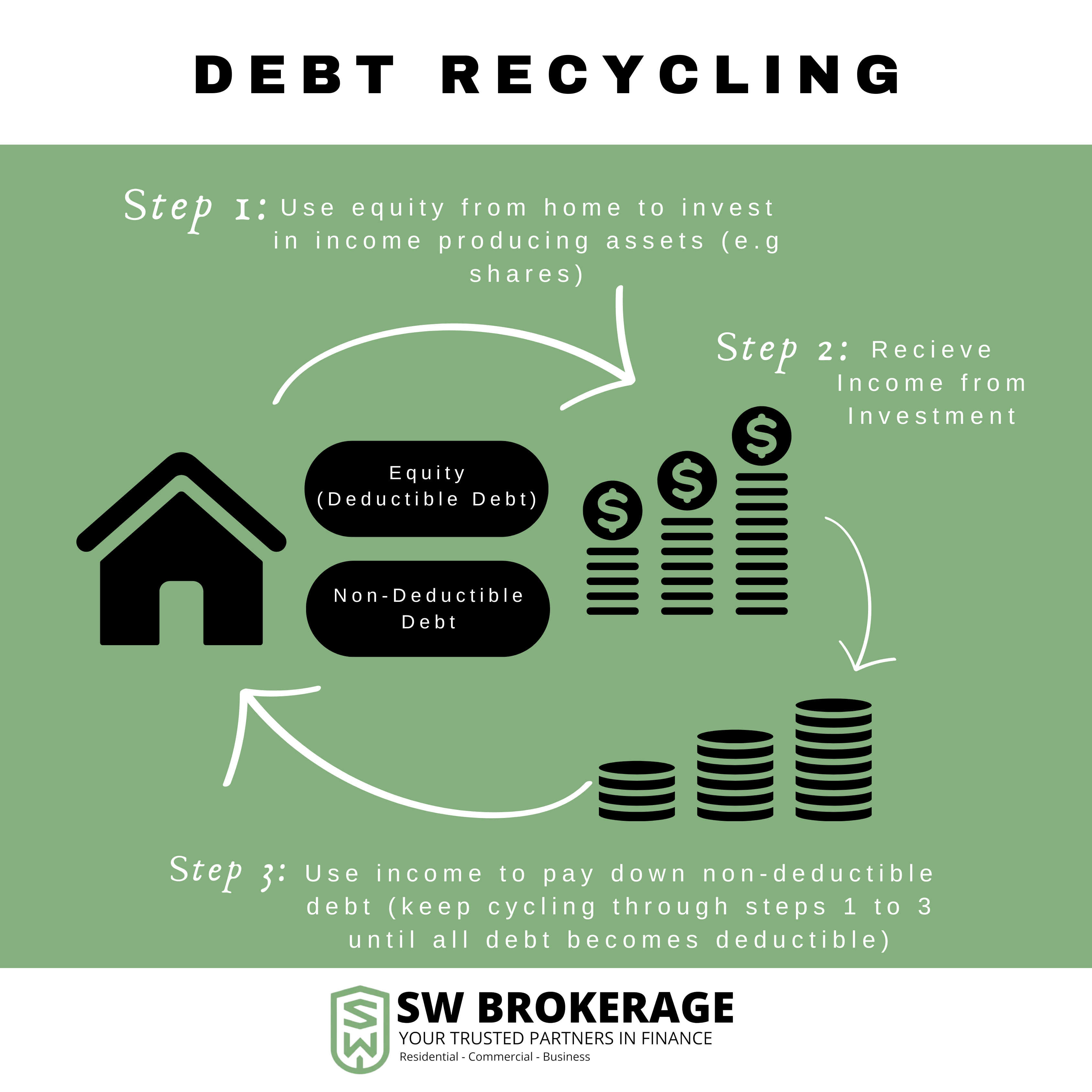

Debt recycling is a wealth-building strategy that involves converting non-deductible personal debt into a separate investment loan to capitalize on tax deductions. Here’s how it unfolds:

- Paying down non-deductible home loan debt: Utilize surplus funds to chip away at your non-deductible mortgage.

- Unlocking equity: Simultaneously, tap into your property’s equity.

- Investing in income-producing assets: Refinance or redraw equity to invest in assets that yield income, thereby converting a portion of non-deductible debt into deductible debt eligible for tax deductions.

Over time, income generated from these investments accelerates the repayment of your original home loan, fuelling the growth of your net worth. Essentially, debt recycling involves utilizing mortgage debt to acquire assets that generate income.

Is Debt Recycling Right for You?

While debt recycling can be a potent wealth-building tool, its suitability varies from person to person. Consider the following factors to determine if it aligns with your financial goals:

- Property Ownership: Debt recycling is particularly advantageous for property owners who can leverage their equity.

- Income Level: High-income earners stand to benefit most from debt recycling due to significant tax savings.

- Risk Tolerance: Assess your comfort level with market volatility and potential losses associated with investing borrowed funds.

Navigating the Risks and Rewards

As with any investment strategy, debt recycling entails risks and rewards. Here’s what you should know:

Potential Risks:

- Market Volatility: Investing borrowed funds exposes you to market fluctuations.

- Rising Interest Rates: Increases in interest rates can strain cash flow, especially with variable-rate loans.

Maximizing Rewards:

- Strategic Asset Selection: opt for assets with robust growth potential to bolster returns.

- Ongoing Portfolio Review: Monitor performance and adjust strategies as needed.

- Professional Guidance: Seek advice from financial experts well-versed in debt recycling strategies.

Getting Started: A Step-by-Step Guide

Ready to embark on your debt recycling journey? Follow these steps:

- Assess Your Borrowing Capacity: Evaluate your financial standing to determine borrowing limits.

- Establish a Flexible Lending Facility: Explore options like lines of credit or split loans for added versatility.

- Prioritize Extra Repayments: Allocate surplus funds to pay down your non-deductible home loan.

- Leverage Equity for Investment: Access equity to invest in assets that generate income.

- Make Informed Investment Choices: Allocate funds to tax-deductible and income-generating assets.

- Leverage Tax Deductions: Maximize savings by claiming deductions on interest payments and associated fees.

Tips for Success

For a seamless debt recycling experience, keep these expert tips in mind:

- Start Small, Scale Up: Begin cautiously and gradually ramp up your debt recycling efforts.

- Craft a Clear Strategy: Define objectives, risk tolerance, and debt reduction timelines upfront.

- Stay Committed: Remain dedicated to long-term goals despite short-term fluctuations.

- Maintain Detailed Records: Track transactions meticulously to maximize benefits.

- Seek Expert Advice: Consult financial professionals for tailored guidance.

In Conclusion

Debt recycling presents property owners with a unique opportunity to fast-track wealth creation and attain financial independence. By converting non-deductible debt into deductible investment debt, individuals can leverage their assets to secure a brighter financial future.

However, successful debt recycling demands meticulous planning, ongoing vigilance, and adaptability to evolving market conditions. With the right approach and expert guidance, debt recycling can unlock new avenues for wealth generation and passive income.

So, if you’re ready to seize control of your financial destiny and optimize your property investment, consider exploring the potential of debt recycling today.

For further insights on maximizing your investment property’s potential, reach out to SW Brokerage for a complimentary consultation on maximizing tax deductions through depreciation with on of our most trusted referral partners who we work in conjunction with.